In some cases, we need to construct a correlation matrix with a predefined set of eigenvalues, which is not trivial since arbitrary symmetric matrices with a given set of eigenvalues may not satisfy correlation constraints (e.g., unit diagonal elements).

A practical method to generate such matrices is based on the Method of Alternating Projections (MAP), as introduced by Waller (2018). This approach iteratively adjusts a matrix between two sets until convergence. It goes like this:

- Normalize the eigenvalues:

- Ensure they are sorted in descending order.

- Scale them such that their sum equals

, the matrix size.

, the matrix size.

- Generate a random orthonormal matrix:

- Construct a random matrix.

- Perform QR decomposition to obtain the orthonormal matrix.

- Iterate until convergence:

- Construct an symmetric positive definite (SPD) matrix using the target eigenvalues and the random orthonormal matrix:

- Clamp values between

and

and  to maintain correlation constraints.

to maintain correlation constraints. - Force all elements on the diagonal to be

.

.

- Clamp values between

- Perform eigen decomposition to extract new eigenvalues and eigenvectors.

- Replace the computed eigenvalues with the target values.

- Compute the distance measure .

- Stop if the distance measure is below a given tolerance.

- Construct an symmetric positive definite (SPD) matrix using the target eigenvalues and the random orthonormal matrix:

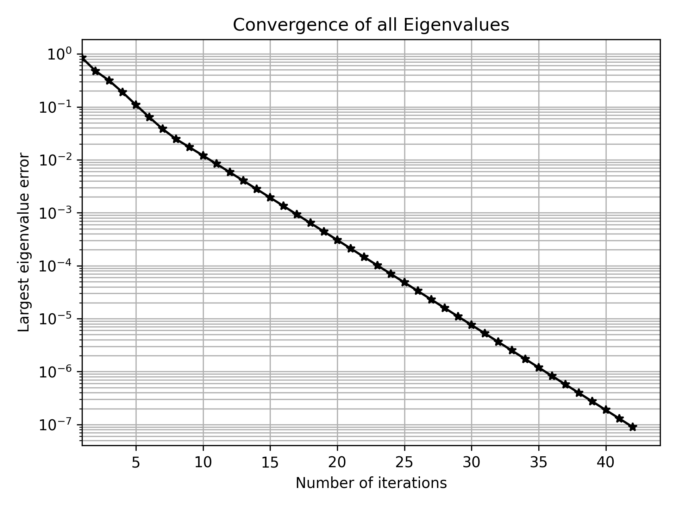

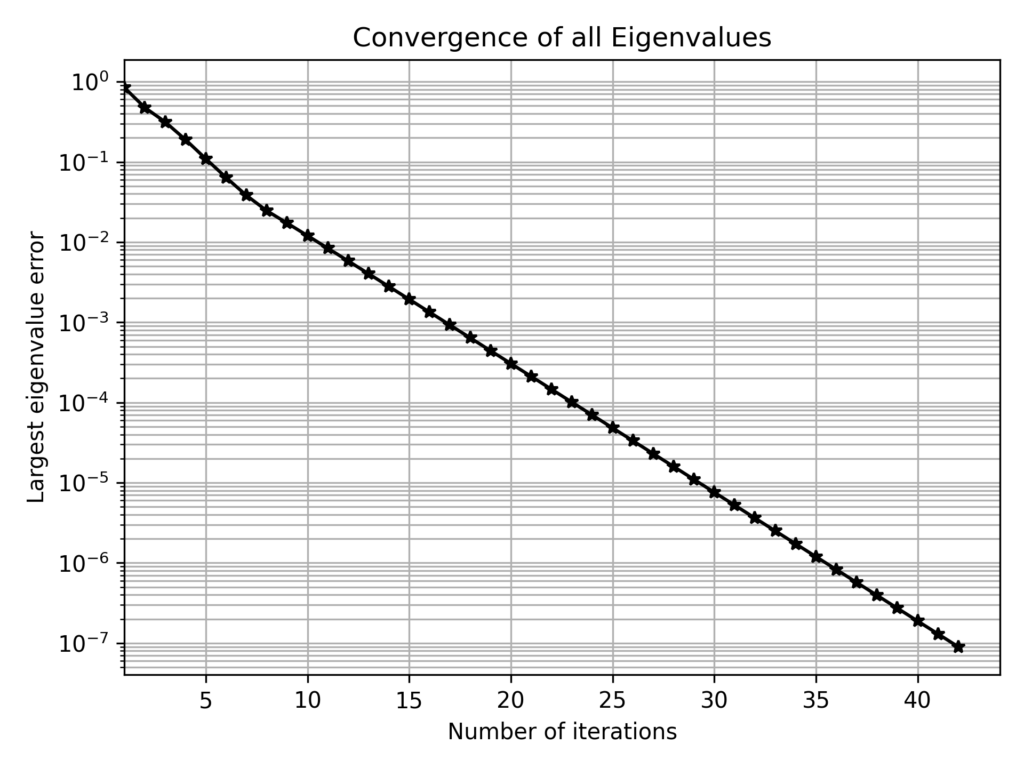

The algorithm seems to converge exponentially fast:

Below Python code!

import numpy as np

def eig_to_cor(eigen_values, eigen_vectors):

"""

Construct a correlation matrix from given eigenvalues and eigenvectors.

"""

cor = eigen_vectors @ np.diag(eigen_values) @ eigen_vectors.T

cor = np.clip(cor, -1, 1) # Ensure valid correlation values

np.fill_diagonal(cor, 1.0) # Force unit diagonal elements

return cor

def cor_to_eig(cor):

"""

Extract eigenvalues and eigenvectors from a correlation matrix,

ensuring they are sorted in descending order.

"""

eigen_values, eigen_vectors = np.linalg.eigh(cor)

idx = eigen_values.argsort()[::-1]

return eigen_values[idx].real, eigen_vectors[:, idx].real

def random_orthonormal_matrix(n):

"""

Generate a random nxn orthonormal matrix using QR decomposition.

"""

Q, _ = np.linalg.qr(np.random.randn(n, n))

return Q

def normalize_eigen_values(eigen_values):

"""

Normalize eigenvalues to sum to the matrix dimension (n) and ensure that they are sorted in descending order.

"""

eigen_values = np.sort(eigen_values)[::-1] # Ensure descending order

return len(eigen_values) * eigen_values / np.sum(eigen_values)

def gen_cor_with_eigenvalues(eigen_values, tol=1E-7):

"""

Generate a correlation matrix with the specified eigenvalues

using the Method of Alternating Projections.

"""

target_eigen_values = normalize_eigen_values(eigen_values)

eigen_vectors = random_orthonormal_matrix(len(target_eigen_values))

while True:

cor = eig_to_cor(target_eigen_values, eigen_vectors)

eigen_values, eigen_vectors = cor_to_eig(cor)

if np.max(np.abs(target_eigen_values - eigen_values)) < tol:

break

return cor

# Example usage:

cor_matrix = gen_cor_with_eigenvalues([3, 1, 1/3, 1/3, 1/3])

print(cor_matrix)

>

array([[ 1. , 0.52919521, -0.32145437, -0.45812423, -0.65954354],

[ 0.52919521, 1. , -0.61037909, -0.65821403, -0.46442884],

[-0.32145437, -0.61037909, 1. , 0.64519865, 0.23287104],

[-0.45812423, -0.65821403, 0.64519865, 1. , 0.38261988],

[-0.65954354, -0.46442884, 0.23287104, 0.38261988, 1. ]])

Waller, N. G. (2018). Generating Correlation Matrices With Specified Eigenvalues Using the Method of Alternating Projections. The American Statistician, 74(1), 21–28. https://doi.org/10.1080/00031305.2017.1401960